Financial review

Introduction

The CPS receives the majority of its resources in the form of Parliamentary funding through the Estimate process. This is supplemented by income, relating predominantly to awards of costs made against convicted defendants and to the Asset Recovery Incentivisation Scheme. The CPS is accountable to Parliament for how it uses these funds and must work within the control totals that Parliament sets. The CPS’ net funding for 2023-24, as voted by Parliament, was £894 million.

This Financial Review explains the budgetary framework within which the CPS operates and sets out how the CPS has performed against its control totals.

Public sector budgeting framework

Like all government departments, the CPS is subject to spending controls set by Parliament and administered by the Treasury. Forward looking spending plans are set through Spending Reviews, which set the level of resources available to departments over the term of the review. Specific control totals for the current financial year are then confirmed through Estimates, which are voted on by Parliament. There are two Estimate publications during the financial year: in May the Main Estimate sets the initial budgets for the year, whilst in February the Supplementary Estimate allows for adjustments to be made and confirms the final budgets against which outturn will be measured. If outturn exceeds the controls voted by Parliament, then this results in an Excess Vote.

Budgets are divided into a number of headings. Firstly, they are categorised under either Departmental Expenditure Limits (DEL) or Annually Managed Expenditure (AME). DEL budgets are set in Spending Reviews and cover the majority of government income and spending. AME budgets apply to more volatile or demand-led areas of income and spending, as determined by Treasury. Some categories of expenditure are automatically treated as AME, including movements in provisions and some types of impairment.

All DEL and AME budgets can be further classified as either Resource or Capital. Resource budgets include most day-to-day income and spending, including delivery of public services, running costs of public sector bodies, and revenue earned. Capital budgets include investment activities, such as purchase and disposal of property, plant and equipment, intangible assets, and some financial assets. Additionally, payment of capital grants and some research and development expenditure is treated as Capital.

Resource DEL budgets are also divided into Programme and Administration budgets. Programme refers to income and spending that relates directly to delivery of departmental objectives and front-line services. All other income and spending is treated as Administration, which covers administrative functions and other overheads. In order to maximise spending on front-line services, departments are set limits on Administration spend. These limits are not voted on by Parliament but are still treated as control totals with any breach resulting in an Excess Vote. Resource AME budgets are always treated as Programme.

Departments are also set a limit on Net Cash Requirement. This is the cash funding requirement arising from Resource and Capital budgets, together with planned movements in working capital. It is effectively the maximum amount of Parliamentary funding that the department can draw down, and breaching this limit results in an Excess Vote.

Control totals are set on a net basis – there are no separate controls on income and expenditure and, subject to Treasury approvals on the retention of income, additional income can be offset against additional expenditure.

A further control on spending is that budgets for depreciation and impairment of assets are treated as ring-fenced. These elements of Resource DEL budgets may not be used for other spending without Treasury approval. However, the ring-fence is not a control voted on by Parliament.

The following are further terms within the budgetary framework:

- Non-budget – Amounts that fall outside the budgetary framework, such as the impact of Prior Period Adjustments.

- Non-voted – Funding that is not voted on by Parliament, such as National Insurance funding.

- Total DEL (TDEL) – The total of Resource DEL and Capital DEL, less depreciation and impairment. This is a measure of overall DEL spending, adjusted to avoid double counting the impact of capital investment in current expenditure.

Outturn against 2022-23 financial control totals

The table below shows the CPS’ performance against our 2023-24 control totals, as agreed by Parliament in the Supplementary Estimate. Further detail on these figures is shown in the Statement of Outturn against Parliamentary Supply and the related notes pages 112-118.

Estimate £000 | Outturn £000 | Variance £000 | |

|---|---|---|---|

| Resource DEL (excluding depreciation) | 796,717 | 783,323 | 13,394 |

| Depreciation | 22,593 | 16,643 | 5,950 |

| Resource DEL | 819,310 | 799,966 | 19,344 |

| Of which administration | 48,034 | 47,712 | 322 |

| Resource AME | 23,950 | 14,517 | 9,433 |

| Capital DEL | 40,100 | 30,859 | 9,241 |

| Capital AME | 10,859 | 6,174 | 4,685 |

There were no breaches of Parliamentary control totals. We are confident that our future spending plans will continue to utilise a high proportion of our budget without the risk of a Parliamentary control total breach.

Significant variances between Estimate and outturn are discussed below.

Significant variances between Estimate and outturn

At the start of the year we estimate our costs for each budget type and we monitor against these throughout the year. Explanations for the variances between Estimate and outturn were as follows:

Resource DEL (£000):

Estimate 819,310 Outturn 799,966

Resource spending (RDEL) is money that is spent on day-to-day resources and administration costs. It includes the hire of agents; prosecution costs; costs of confiscating the proceeds of crime; capacity building in the criminal justice system; support of voluntary sector organisations within the criminal justice system; and depreciation. The RDEL funding is shown net of income, including that arising from costs awarded to the CPS in court or received through the Recovered Assets Incentivisation Scheme.

The majority of our spend goes towards our internal workforce, in particular Legal and Frontline pay. Together with the cost of the highly valued work undertaken on behalf of the CPS by the external Bar and spend towards supporting victims and witnesses attending court, this accounts for over 80% of CPS expenditure.

During the course of the year, the CPS faced significant pressure from prosecution costs, particularly as these costs are dependent on activity levels which are outside of CPS control. This accounted for £4.0m of RDEL underspend in 2023-24.

To mitigate financial pressures faced during 2023-24, the CPS implemented additional spending controls. This resulted in reductions in IT services and projects spend, staff and other spend, which contributed to a £5m RDEL underspend.

Additionally, the CPS benefited from successes in recovering £3.7m more income than forecast, largely as a result of a higher value of costs awarded to the CPS and via the Asset Recovery Incentivisation Scheme.

CPS’ spend on depreciation also accounted for £6.0m of RDEL underspend. This was a result of both changes to timescales in relation to IT systems, as well as delays by Government Property Agency in the signing of intra-government tenancy agreements following leases agreements signed by GPA, meaning the CPS was unable to recognise the properties under IFRS 16.

These key elements combined accounted for a substantial proportion of the underspend. Whilst the level of underspend is higher than in the previous financial year, the distribution of our Resource DEL spend is now in line with HM Treasury ringfences.

Resource AME (£000):

Estimate 23,950 Outturn 14,517

Annually Managed Expenditure (AME) is uncertain in nature and difficult to predict.

The CPS recognises an allowance for expected losses relating to costs awards income, which scores against the AME budget. In previous years, the allowance has predominantly been based on historic trends. However, since the 2021-22 financial year, there have been a few substantial changes which have increased the unpredictability of collection rates (how much cash is subsequently collected in relation to the costs awarded to the CPS). The first of these changes relates to amended legislation whereby costs awarded which are collected by the Department for Work and Pensions (DWP) on behalf of CPS are expected to be collected at a slower rate. As this is a comparatively recent change, at the time of the Supplementary Estimate the impact of the change was still not fully known, increasing the level of uncertainty in the Estimate.

Secondly, there is a legal hierarchy for recovery, in which cash collected from offenders is used to pay compensation and the Victim Surcharge before the CPS receives the costs it has been awarded. During the 2022-23 financial year, there was an increase to rates for the Victim Surcharge and consequentially more cash is required to be collected from offenders to pay off the Victim Surcharge before the CPS will receive the cash for costs awarded. Therefore, the increase in Victim Surcharge rates is expected to reduce the amounts collected relating to costs awarded to the CPS, increasing the expected losses relating to costs awards income. At the time of the Supplementary Estimate, there was limited data to assess the impact of the change, significantly increasing the uncertainty of the estimate.

In addition, estimated future cash flows are discounted using the HM Treasury rate for financial instruments. The discount rate for the 2023-24 financial year is not published until after Supplementary Estimates are submitted. Given the increases in interest rates over the last few financial years, it is now more difficult to predict the discount rate.

The combination of all of the above factors meant that there was a significant level of uncertainty in the estimate at the time of submitting the Supplementary Estimate. Although, there was an increase in allowance of £5.4m during the year, this was significantly lower than the forecasted value of £10.9m.

As part of the Supplementary Estimate, the CPS requested an additional £10.0m for an impairment as a result of an expected recommendation by HMCTS to revise the scope of the interface between the CPS’ Case Management System and HMCTS’ Common Platform system. The value of the impairment was subsequently quantified to be £10.4m. This impairment scores as AME as the interface will now be used for a lower specification purpose than was originally intended as a result of the subsequent decision to implement the HMCTS recommendation.

However, this small overspend was offset by the writing back of a number of provisions for both legal cases and dilapidations that are no longer required, as well as by the utilisation of provisions used in year.

The combined impact of all the elements detailed above resulted in a large Resource AME underspend.

Capital DEL (£000):

Estimate 40,100 Outturn 30,859

At the time of the Supplementary Estimate, expectations based on discussions with GPA were that leases on a number of properties would be completed, with corresponding intra-government agreements signed between GPA and the CPS before the end of the financial year. As not all of these agreements transpired in line with the plan, this resulted in a significant underspend of Capital DEL. However the variance represents a significant improvement in comparison to 2022-23 when the variance was £26.8m.

Capital AME (£000):

Estimate 10,859 Outturn 6,174

In order to comply with IFRS 16 – Leases, an estimate of any dilapidations liability is required to be capitalised as part of the corresponding right-of-use asset value. As a result of expected agreements not being signed with GPA in 2023-24, corresponding dilapidation provisions, which would score as Capital AME, were not required in 2023-24.

Net Cash Requirement (£000):

Estimate 841,017 Outturn 807,680

The variance between the net cash requirement estimate and outturn is largely as a result of variances outlined above.

Reconciliation of budget outturn to financial statements

The budget headings used in Estimates are designed to support the treatment of expenditure in the UK’s national accounts, whereas the financial statements in departmental accounts are prepared in accordance with International Financial Reporting Standards (IFRS). In most cases, transactions are treated similarly in both frameworks, but there are some misalignments. For instance, the payment of capital grants to external bodies is treated as current expenditure in financial statements, but for Estimate purposes are reported against Capital budgets.

The following diagram illustrates how the CPS’ budget outturn above differs from the amounts reported in the financial statements on pages 126 to 129.

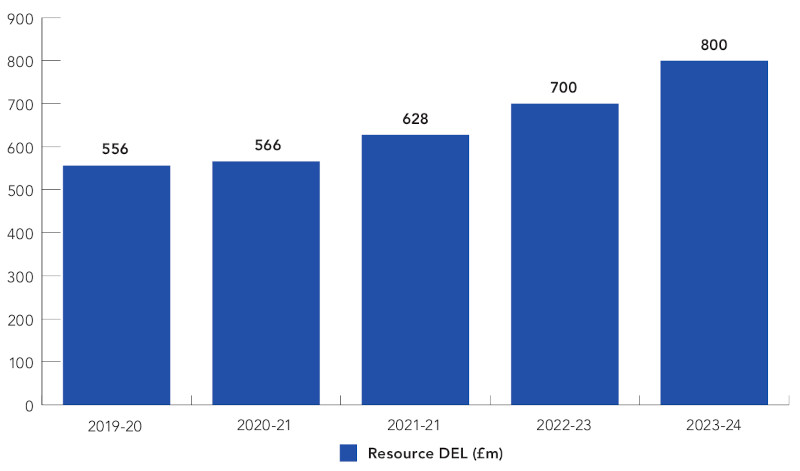

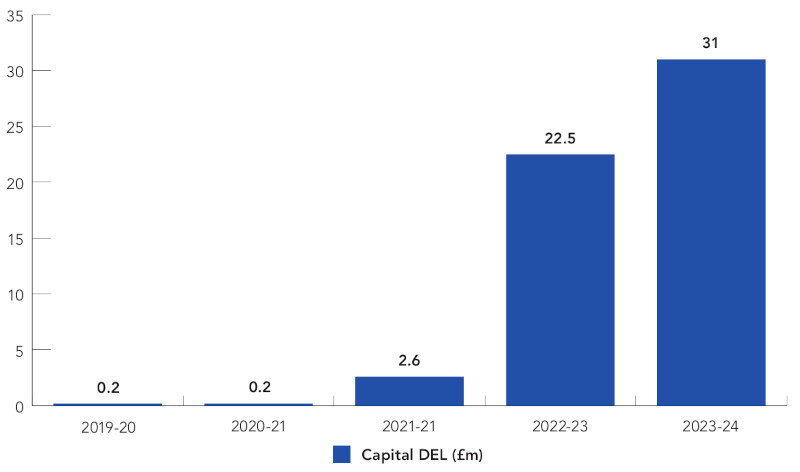

Budget outturn trend analysis

The following charts show the CPS’ Resource DEL and Capital DEL outturn for the past five years.

| Period | 2019-20 | 2020-21 | 2021-22 | 2022-23 | 2023-24 |

|---|---|---|---|---|---|

| Resource DEL (£m) | 556 | 566 | 628 | 700 | 800 |

| Capital DEL (£m) | 0.2 | 0.2 | 2.6 | 22.5 | 31 |

Payment to suppliers and witness expenses

The CPS is committed to paying bills in accordance with agreed contractual conditions or, where no such conditions exist, within 30 days of receipt of goods or services or the presentation of a valid invoice, whichever is the later. The CPS also seeks to pay all expenses to prosecution witnesses within five working days of receipt of a correctly completed claim form.

In 2023-24 the CPS settled 96.2% of undisputed invoices and staff and witness expense claims within 10 days of receipt (2022-23, 94.9%). The CPS paid £nil (2022-23, £nil) in interest due under the Late Payment of Commercial Debts (Interest) Act 1998.